The Headlines Are Screaming—But Should You Panic?

You've probably seen the news: MSCI is changing its index rules to exclude newly issued shares from crypto treasury companies like MicroStrategy (MSTR). Financial media is calling it a "blow" to the Bitcoin buying machine. Some are even saying it's the end of MSTR's "infinite money glitch."

But here's the thing that most people are missing: MSTR doesn't primarily fund its Bitcoin purchases through stock issuance. Their main engine is something called Convertible Bonds (CB), and that market is completely unaffected by MSCI's decision.

So before you panic or start reshuffling your portfolio, let's take a deep breath and look at the actual numbers. Because the reality is a lot less dramatic than the headlines suggest.

What Actually Changed?

First, let's understand what MSCI actually did.

The Old Rule: When a company in the MSCI index issues new shares (through an At-The-Money offering, or ATM), the index automatically adjusts to include those shares. This means passive funds tracking the index—think BlackRock, Vanguard, and hundreds of others—are forced to buy the new shares to maintain their index weighting.

This created what traders called "free money" or an "auto-bid." MSTR could issue stock, and passive funds would automatically buy it. The money from selling that stock would then go straight into buying Bitcoin.

The New Rule: MSCI will now delay or exclude newly issued shares from crypto treasury companies. This means passive funds won't be forced to buy the new stock immediately. The automatic bid is gone.

Sounds bad, right? Let's look deeper.

MSTR's Funding Structure: The Real Story

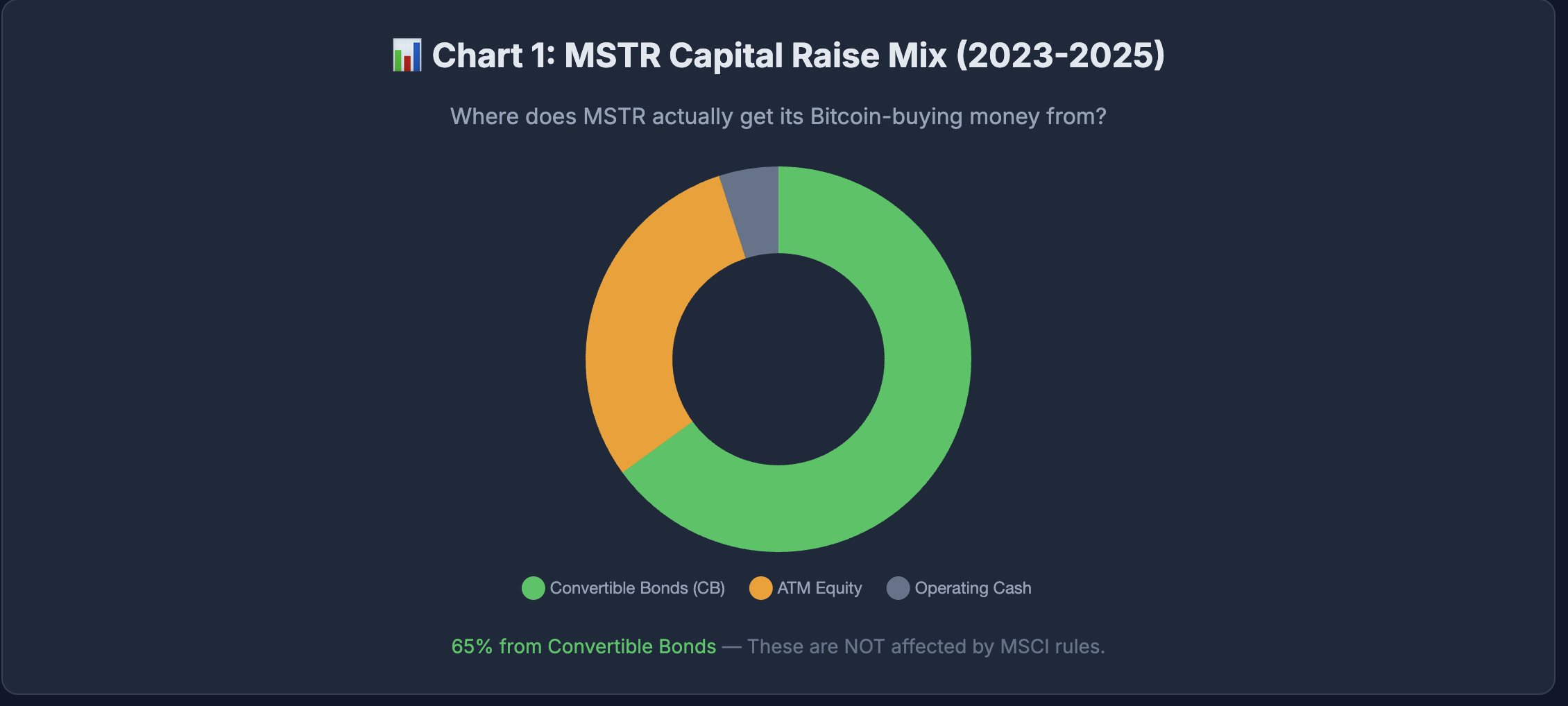

Here's the chart that everyone needs to see:

Look at that breakdown. About half of MSTR's funding comes from Convertible Bonds (CB)—roughly $7B annually. The other half comes from ATM stock issuance—also about $7B, and this is the part affected by the MSCI rule change.

Let's break down what these funding sources actually are:

Convertible Bonds (CB) - ~$7B Annually

These are the crown jewels of MSTR's funding strategy. A Convertible Bond is essentially a loan that can convert to stock later if the stock price goes up. The magic? MSTR offers these bonds at near-zero interest rates because the conversion option is so valuable to investors.

Who buys these bonds? Hedge funds doing volatility arbitrage. They don't care about MSCI index weightings at all. They're trading the volatility embedded in the conversion option. The MSCI rule change doesn't affect them one bit.

ATM Equity (Stock Issuance) - ~$7B Annually

This is where MSTR sells new stock directly into the market at current prices. This is the part affected by the MSCI change. Without the automatic passive buying, the stock may face more selling pressure when MSTR issues new shares.

But here's the key insight: even within this 30%, not all of it was going to passive funds. Active managers, retail traders, and institutions were also buying. The MSCI change only removes the passive portion of this demand—maybe 15-20% of the ATM issuance was being absorbed by index trackers.

Operating Cash Flow - 5% of Funding

MSTR still has a software business that generates modest cash flow. It's not significant compared to their Bitcoin buying, but it exists.

The Passive Buying Power: Before vs. After

Let's quantify exactly how much passive buying is being lost.

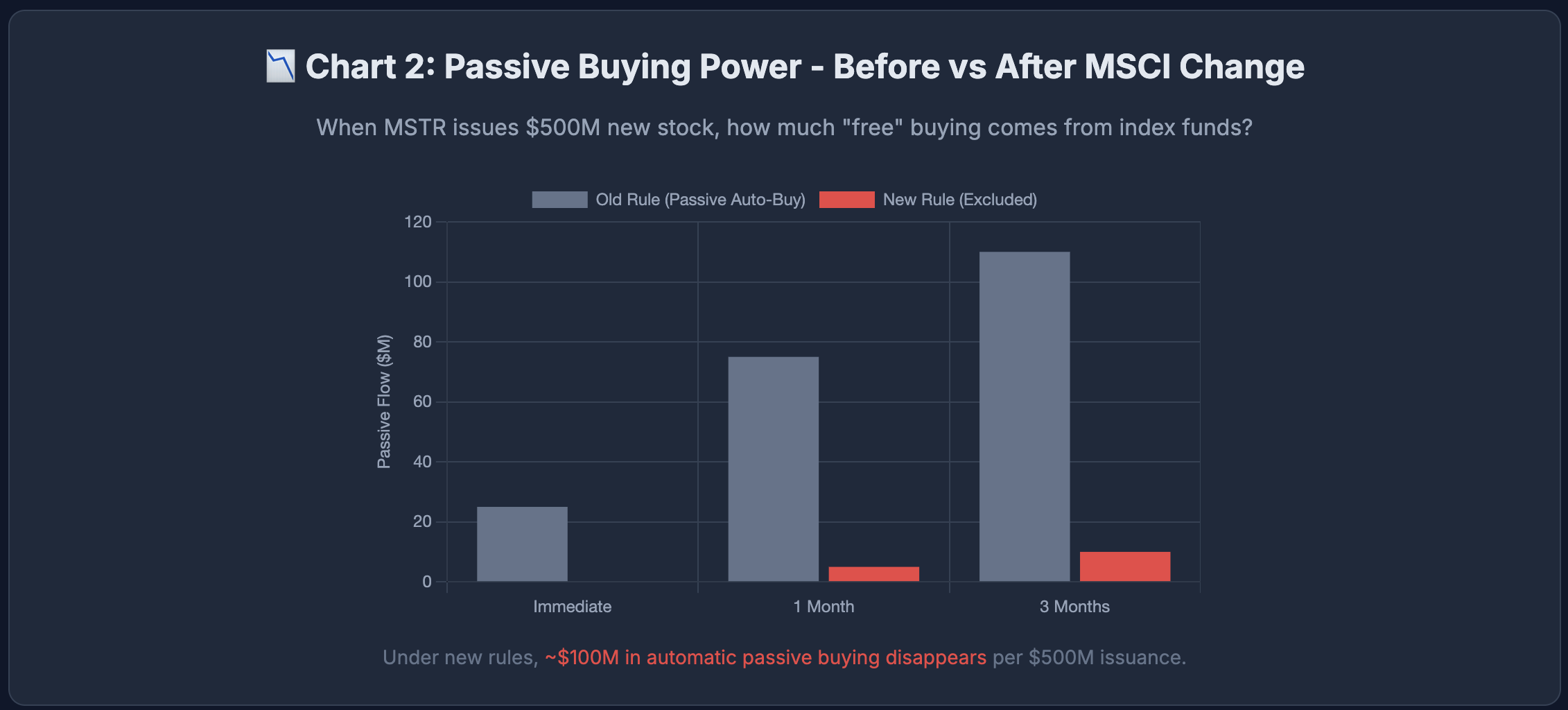

This chart shows what happens when MSTR issues $500M in new stock:

Old Rule: Over time, about $110M in passive buying would flow into the stock as index funds rebalanced—approximately 22% of the issuance.

New Rule: That passive buying drops to nearly zero. Maybe $10M at most, and only if MSCI eventually includes the shares after a delay.

So we're talking about roughly $100M fewer dollars flowing into MSTR stock per $500M issuance. Is that bad? Yes. Is it catastrophic? Let's compare it to the full picture.

Bitcoin Buying Sources: The Complete Picture

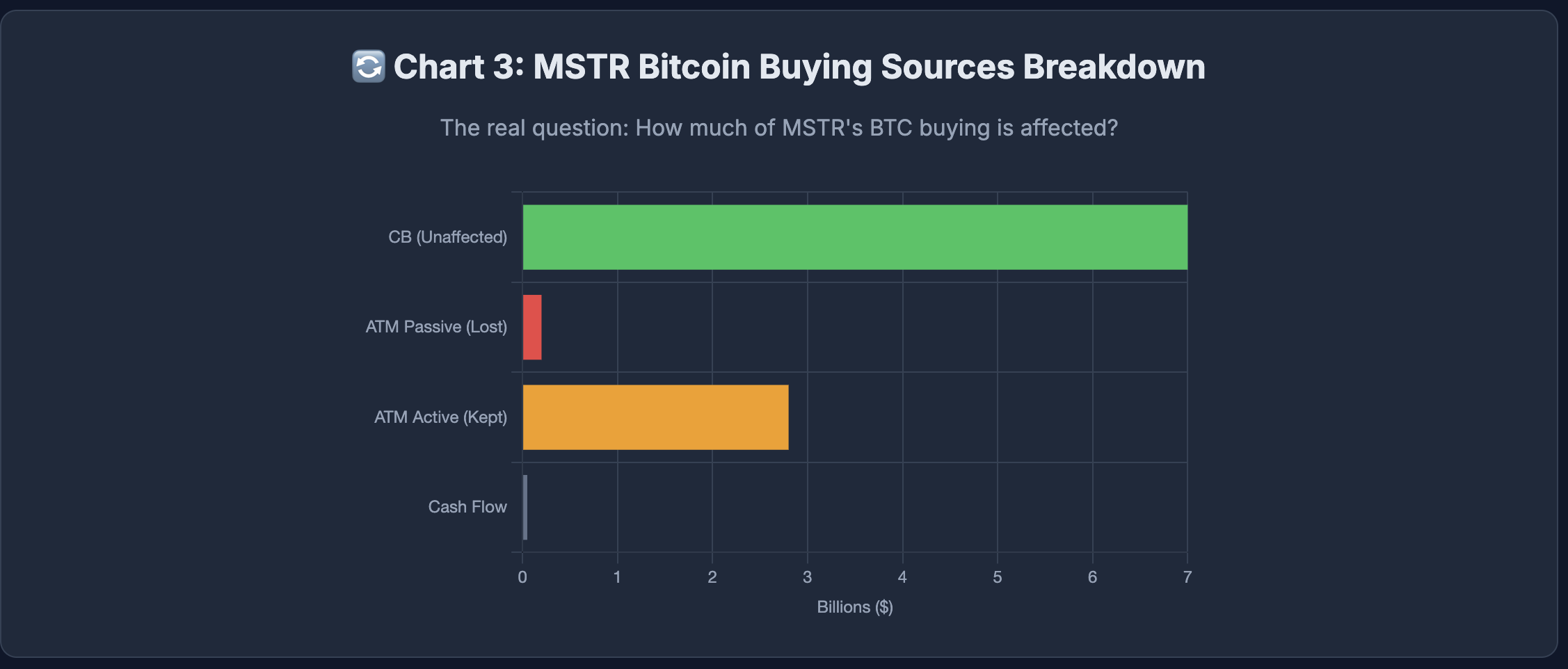

Now let's zoom out and look at MSTR's total Bitcoin buying power:

Look at those numbers:

CB (Unaffected): $7.0 Billion — This is MSTR's edge. The CB market remains wide open and completely unaffected.

ATM Passive (Lost): $1.0 Billion — This is what's being lost. About 15% of the $7B ATM issuance was going to passive index funds—roughly $1B annually.

ATM Active (Kept): $6.0 Billion — Active managers, retail, and institutions still purchase MSTR stock. They're not forced by index rules, but many want exposure to MSTR's Bitcoin strategy.

The total annual Bitcoin buying power was roughly $14 billion. We're losing about $1 billion of that—approximately 7% of the total.

Seven percent is significant—but it's not catastrophic.

The key point: the CB engine ($7B) is still running at full throttle, and active buyers ($6B) aren't going anywhere.

Historical Context: CB Has Always Been King

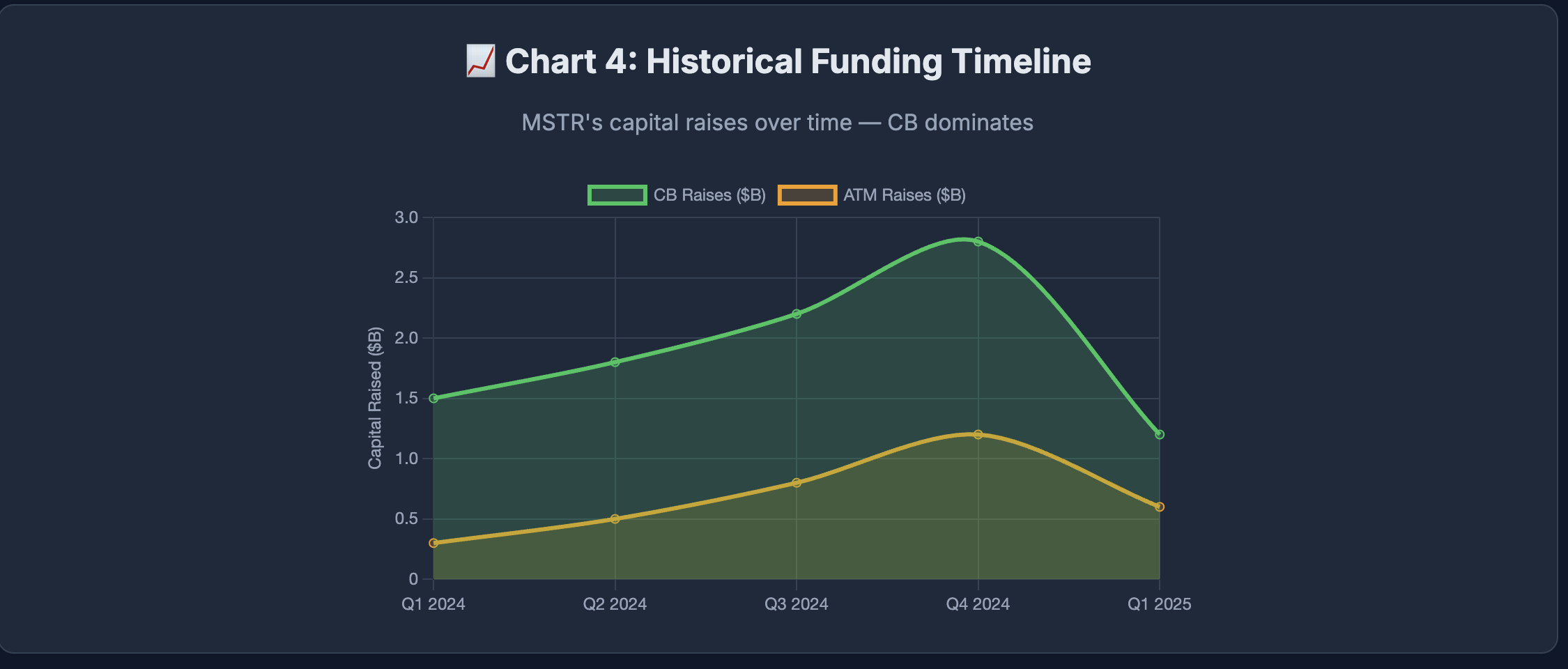

Let's look at how MSTR has raised capital over the past few quarters:

The green area (Convertible Bonds) consistently dominates the orange area (ATM Equity). In Q4 2024, MSTR raised nearly $3 billion in CB alone versus about $1.2 billion in ATM.

This isn't new behavior in response to the MSCI change—this has been MSTR's strategy all along. Michael Saylor has always preferred CB because:

- Near-zero interest rates: The conversion option is so valuable that CB investors accept almost no interest.

- No immediate dilution: Until the bonds convert, existing shareholders aren't diluted.

- Huge hedge fund demand: The volatility arbitrage opportunity attracts institutional capital.

The ATM issuance has always been a "nice to have" bonus, not the core strategy.

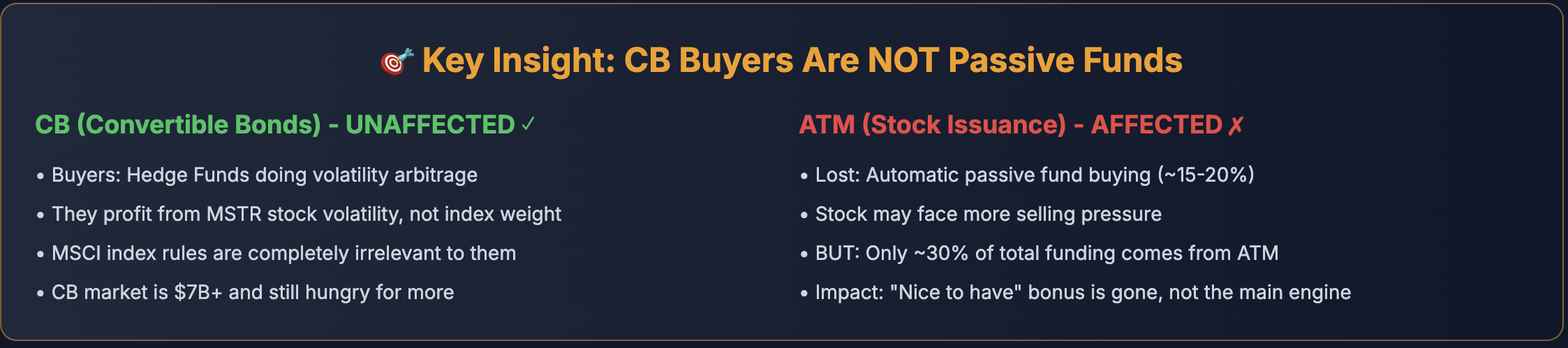

The Key Insight: CB Buyers Don't Care About MSCI

This is the most important point in this entire analysis:

CB Buyers (Unaffected):

- Hedge funds doing convertible arbitrage

- They profit from MSTR's stock volatility, not its index weight

- MSCI rules are completely irrelevant to their strategy

- The CB market is still hungry—there's $7B+ in demand

ATM Buyers (Partially Affected):

- Lost: Automatic passive fund buying (~15-20% of ATM)

- Kept: Active managers, retail, and institutional buyers who want Bitcoin exposure through MSTR

- Net impact: Stock may trade at slightly lower premiums, but the core demand remains

What About Other Bitcoin Treasury Companies?

Here's where the story gets more interesting. While MSTR is relatively insulated because of its CB focus, other players are more vulnerable.

Bitcoin Mining Companies (MARA, RIOT, etc.):

These companies don't have MSTR's credibility in the CB market. They rely much more heavily on ATM issuance. For them, losing the passive bid could actually hurt—their cost of capital may rise.

Smaller Crypto Treasury Plays:

Some newer companies that copied the MSTR playbook are going to struggle. Without the passive bid and without access to cheap CB financing, their Bitcoin accumulation strategies become less attractive.

In a way, the MSCI rule change might actually benefit MSTR by widening its competitive moat. It's harder for copycats to catch up when the "easy money" from passive buying is gone.

The Flywheel: Slightly More Friction, But Still Spinning

Let's talk about the famous MSTR "flywheel"—the self-reinforcing cycle that drives Bitcoin buying:

The Old Flywheel:

Stock price rises → Market cap increases → Index weight increases → Passive funds buy more → Stock price rises → MSTR issues more stock → Buys more Bitcoin → Bitcoin price rises → Stock price rises → Repeat

The New Flywheel:

Same cycle, but the "Passive funds buy more" step is weakened. The wheel still spins, but with slightly more friction.

Think of it like losing one gear in a complex machine. The machine still works, but it's not quite as smooth.

The Verdict: "Easy Mode is Over"

Here's the honest assessment:

What We Lost:

- ~$1B in annual automatic passive buying

- A "nice to have" tailwind that made ATM issuance slightly easier

- Some downside protection when MSTR issues new stock

What We Kept:

- The $7B+ Convertible Bond engine—completely unaffected

- Active demand from institutions and retail who want Bitcoin exposure

- MSTR's unique position as the most credible Bitcoin treasury company

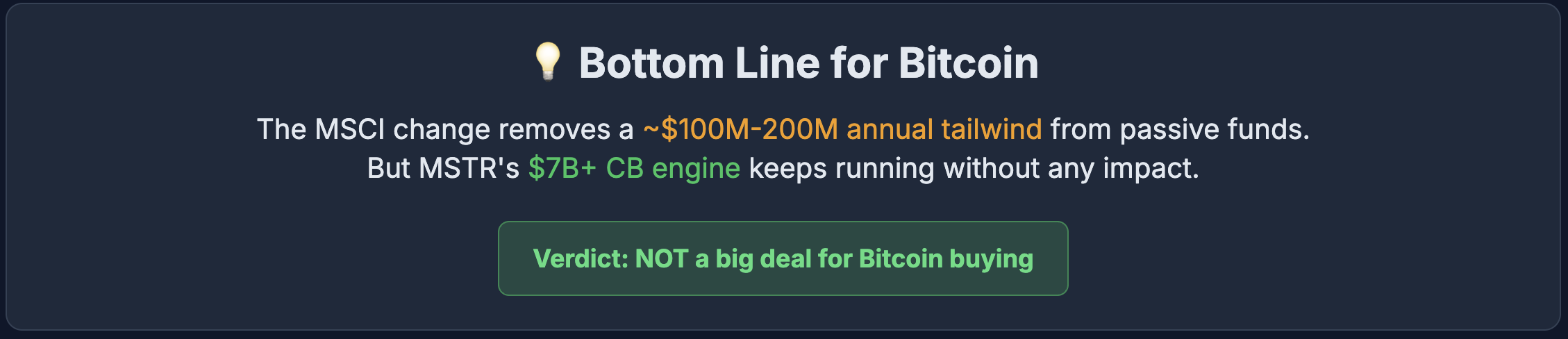

The Bottom Line:

The MSCI change is real and meaningful—losing ~7% of buying power is not trivial. But it's far from catastrophic. Think of it as losing a tailwind, not crashing the plane. MSTR's Bitcoin buying will continue—maybe at 93% of its previous pace instead of 100%.

For Bitcoin holders and MSTR investors, this is a minor adjustment, not a paradigm shift.

What Should Traders Watch?

If you're actively trading around MSTR or Bitcoin, here's what to monitor:

1. MSTR Premium to NAV:

Watch how MSTR's stock price compares to the value of its Bitcoin holdings. Without passive buying, the premium may compress slightly. This could create buying opportunities.

2. CB Issuance Announcements:

When MSTR announces a new Convertible Bond offering, that's real new capital entering the Bitcoin market. These announcements are more important than ever.

3. ATM Usage:

Track how aggressively MSTR uses its ATM facility. If they scale back ATM issuance and lean more on CB, the MSCI change becomes even less relevant.

4. Copycats Struggling:

Watch smaller Bitcoin treasury companies. If they can't raise capital as easily, MSTR's dominance increases. This could actually be bullish for MSTR's competitive position.

The Bigger Picture: Crypto Growing Up

In a strange way, the MSCI rule change is a sign that crypto is maturing.

Think about it: index providers are now making specific rules for crypto companies. That means they consider crypto significant enough to regulate separately. A few years ago, MSCI probably wouldn't have cared.

Yes, this particular rule is restrictive. But the broader trend is one of increasing recognition. Crypto assets are becoming serious enough that traditional finance has to adapt its rules to accommodate them.

The passive buying loophole was always a bit of a hack. It was never going to last forever. Now the market is moving to a more sustainable model where capital flows into Bitcoin because people want to buy it, not because they're forced to by index mechanics.

Final Thoughts

The headlines about the MSCI rule change are overblown. Here's the reality:

- MSTR's main funding source (CB) is unaffected

- Lost passive buying is ~7% of total buying power (~$1B/year)

- The flywheel still spins, just with slightly more friction

- Copycats may struggle, strengthening MSTR's moat

Should you panic? No.

Should you adjust your expectations slightly? Maybe.

Is this the end of the Bitcoin buying machine? Absolutely not.

The Convertible Bond market remains wide open. Hedge funds are still lining up to buy MSTR's debt. And as long as that's true, the Bitcoin buying continues.

"Easy Mode" might be over. But the game is still very much being played.