The Price Isn't Universal

Here's a question that keeps sophisticated traders up at night: You're watching Bitcoin options on your screen. Deribit shows a $500 premium for a specific call. You check CME—the same strike, same expiry—but the implied volatility suggests a different price. Which one is "correct"?

The answer: Both. And neither.

In crypto derivatives, price isn't a universal truth. It's a consensus, and that consensus is often fractured across different venues. For passionate crypto traders, understanding spot price is just the beginning. The real edge lies in understanding Market Structure—the invisible mechanics that determine where liquidity lives, where it dies, and when it disappears entirely.

The Tale of Two Markets

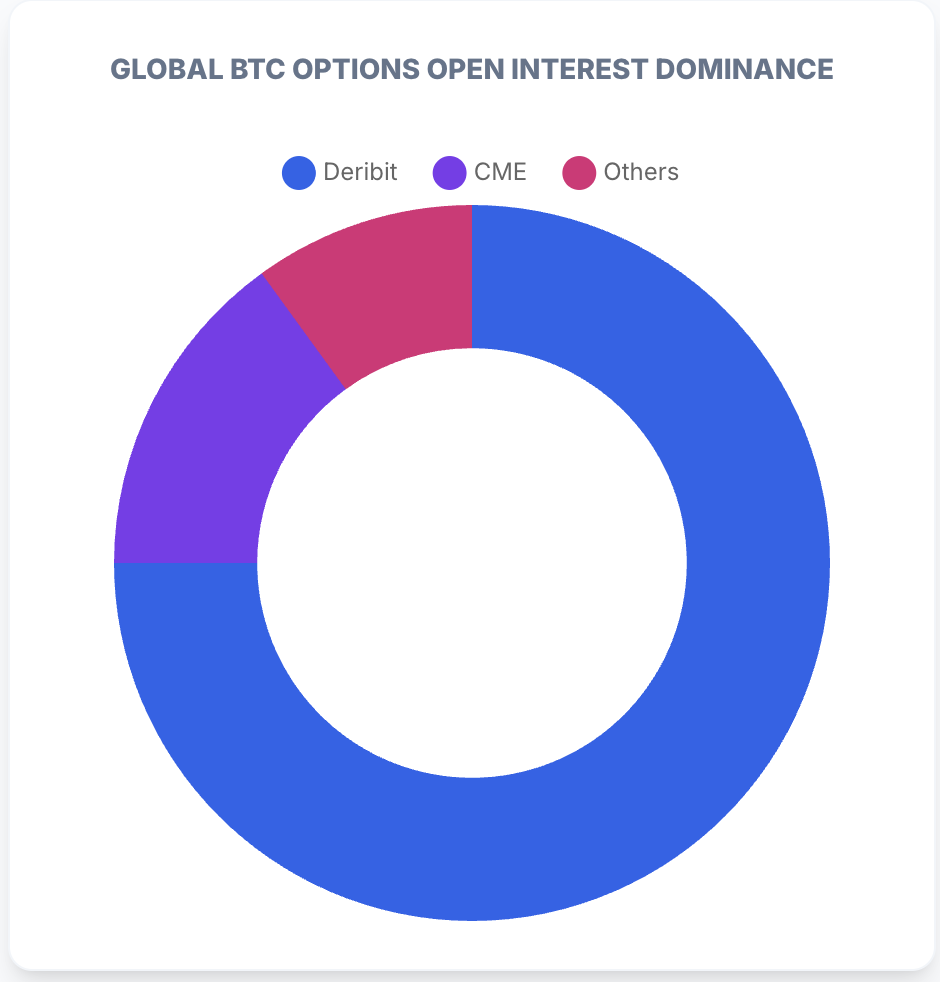

Bitcoin options volume is dominated by two giants: Deribit (the crypto-native offshore king) and CME (the regulated institutional venue). This isn't just a geographic split—it's a structural divide that creates what we call Liquidity Fragmentation.

Why This Split Matters

Deribit operates 24/7, populated by crypto-native funds, miners, and retail pro-traders. It's fast, it's liquid, and it never sleeps.

CME is the playground of traditional finance (TradFi) asset managers. It closes strictly on weekends. It's regulated, it's slower, and it requires institutional infrastructure to access.

Because capital cannot move instantly between these two silos—due to banking hours, settlement times, and regulatory friction—arbitrage inefficiencies persist. You might see a call option priced at $500 on Deribit while a structurally similar contract on CME implies a different volatility. This isn't an error. It's the cost of fragmented liquidity.

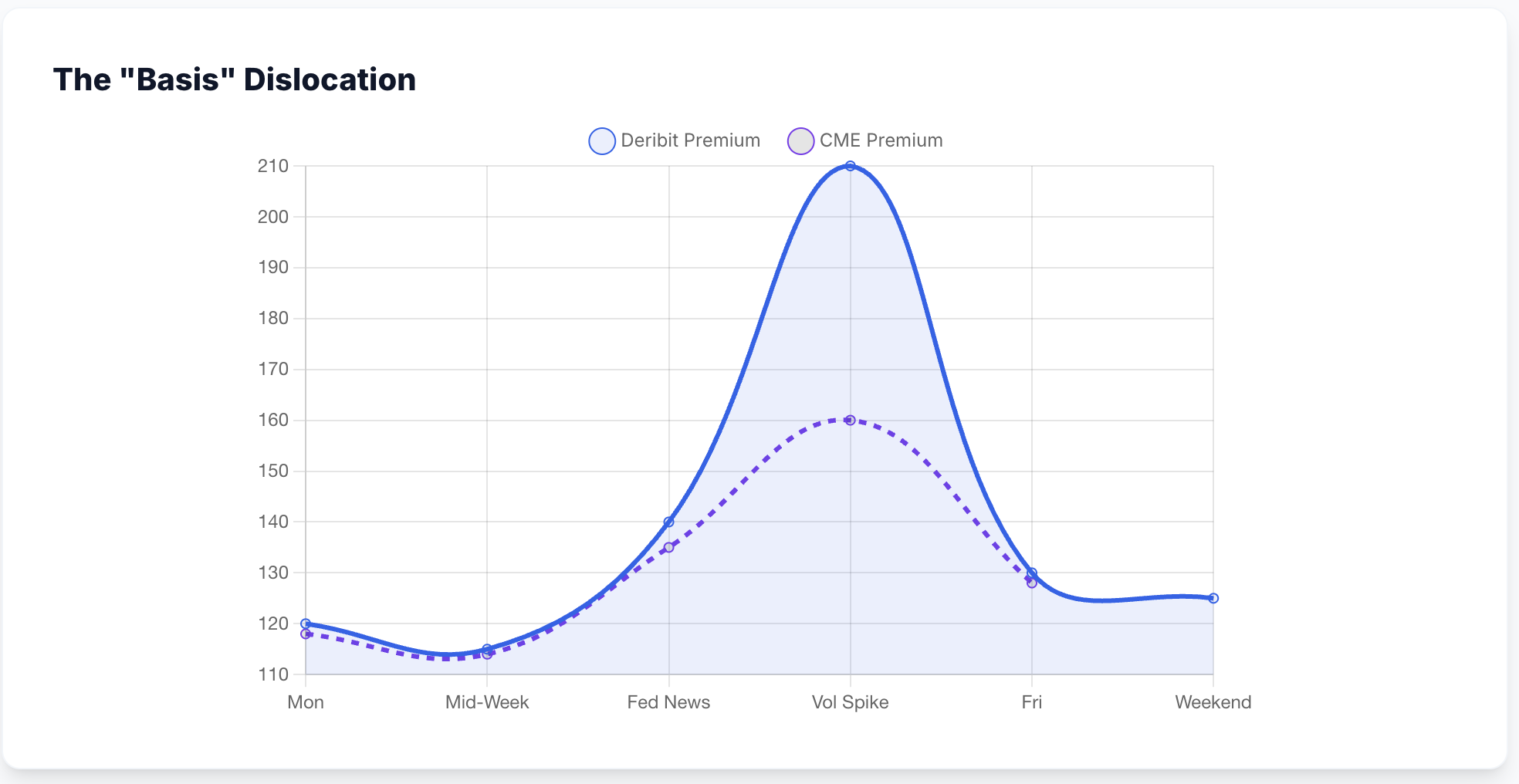

The Basis Dislocation

When markets move violently, the price of "forward" liquidity disconnects. Traders call this the "Basis Spread"—the premium difference between offshore and regulated futures during high volatility events.

What This Means for You:

- When the spread widens, you might be paying a premium on one exchange without realizing it

- Arbitrageurs with access to both venues can profit from these inefficiencies

- Retail traders stuck on one platform are often on the wrong side of the trade

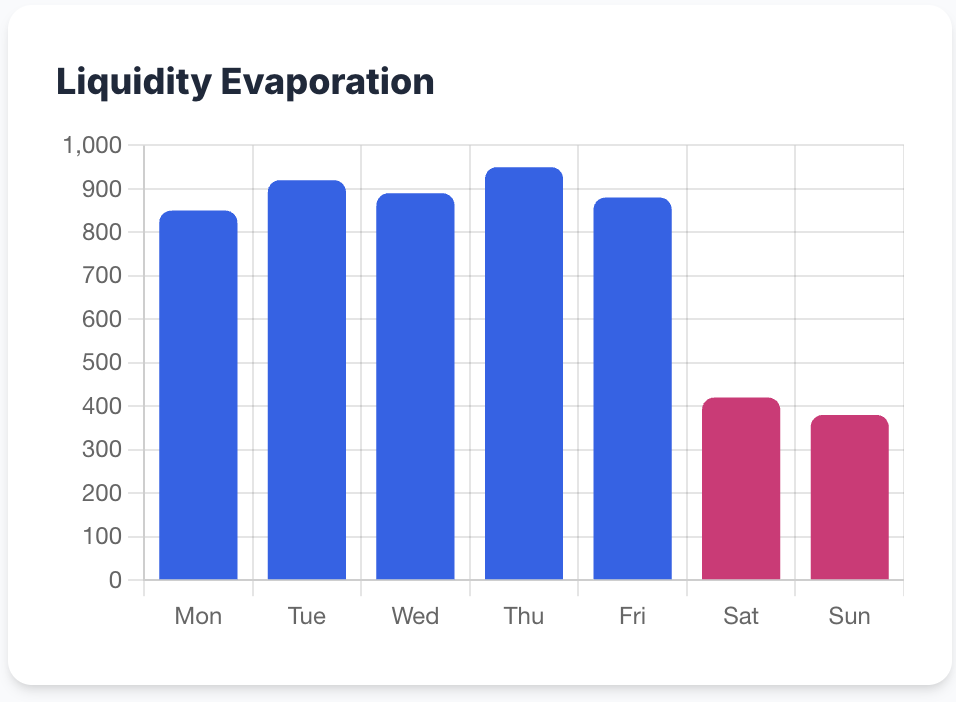

The Weekend Gap: When Institutions Sleep

Crypto markets never close, but banking does. This creates a unique phenomenon: The Weekend Gap.

From Friday 5 PM EST to Sunday 6 PM EST, institutional liquidity providers (LPs) widen their spreads or leave the order book entirely on CME. Even on crypto-native exchanges like Deribit, volumes drop significantly.

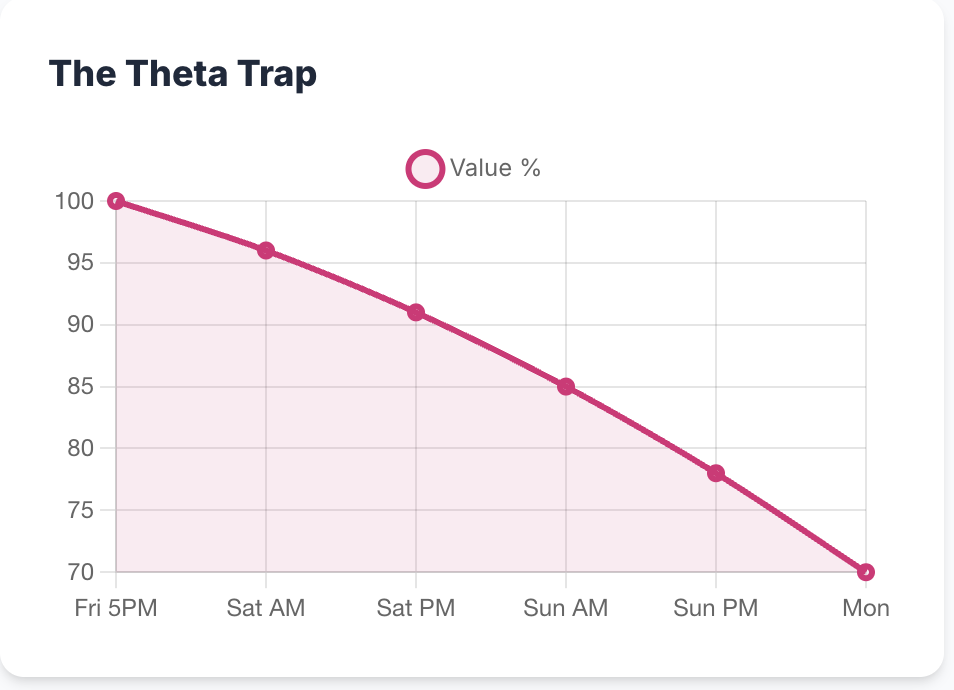

The Theta Trap

For option holders, time is the enemy. Theta (Time Decay) doesn't take the weekend off. If you hold a short-dated option (weekly or daily expiry) over the weekend, you're paying full "time rent" for a period where price realization (volatility) is statistically lower.

Think of it this way: You're paying rent for an apartment you can't use. The clock keeps ticking, but the market isn't moving enough to justify the cost.

Three Weekend Dangers

1. Accelerated Decay

Theta decay accelerates as expiration approaches. Holding 0DTE (zero days to expiry) or weekly options through a low-volatility weekend is statistically a negative expected value (EV) play. You're bleeding premium for nothing.

2. Whale Games

With thin order books, it takes less capital for "Whales" to push price around. They often hunt stop-losses before Monday open, knowing retail traders are asleep or unable to react quickly.

3. Hedging Cost Spike

If you need to hedge over the weekend, implied volatility may spike due to lack of liquidity. You're forced to pay higher premiums precisely when you need protection most.

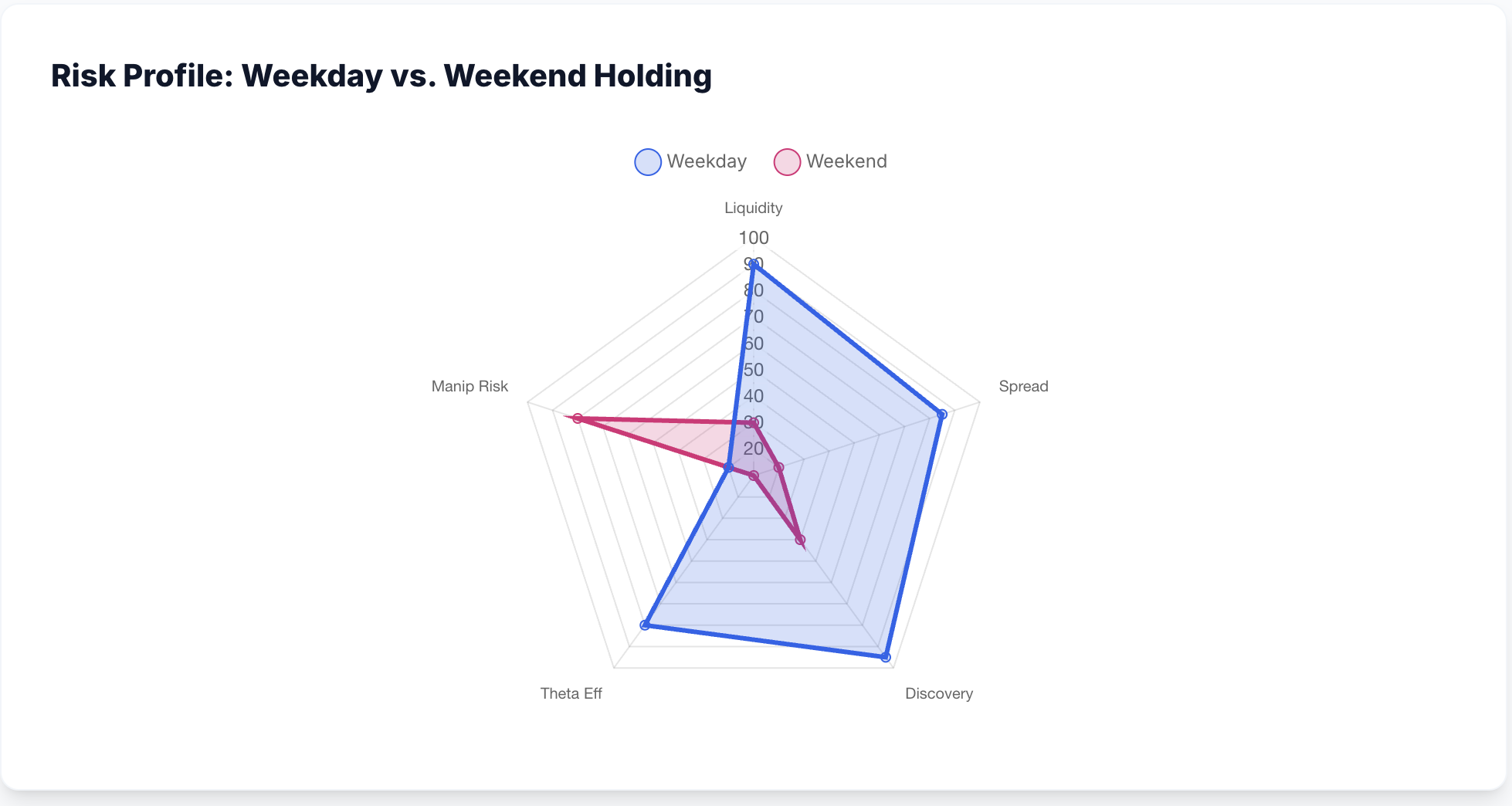

Risk Profile: Weekday vs. Weekend

The difference between holding options during the week versus over the weekend is stark. Here's how the risk profile changes:

Weekday Trading: High liquidity, tight spreads, efficient price discovery, reasonable theta costs, low manipulation risk.

Weekend Trading: Low liquidity, wide spreads, poor price discovery, terrible theta efficiency, high manipulation risk.

How to Protect Yourself

Strategy 1: Close Before Friday

If you're holding short-dated options (7 days or less), consider closing your position before Friday 4 PM EST. The theta bleed over the weekend often exceeds any potential upside from holding.

Strategy 2: Use Longer Expiries

Monthly options are less affected by weekend theta decay. If you must hold over the weekend, use contracts with at least 30 days to expiry.

Strategy 3: Monitor the Spread

Before entering a trade, check the Deribit-CME spread. If it's unusually wide, you're likely paying a premium. Wait for the spread to normalize or choose a different venue.

Strategy 4: Avoid Weekend Entries

Don't open new option positions on Saturday or Sunday. You're buying into the worst liquidity conditions of the week. Wait for Monday when institutional flow returns.

What Blockskew Is Building

Understanding these mechanics is just the beginning. At Blockskew, we're developing tools to help you navigate this fragmented landscape:

The Arb-Gap Monitor

A live dashboard widget that calculates real-time implied volatility spread between CME and Deribit. Get alerts when offshore markets are "overheating" relative to regulated norms.

Weekend Theta Heatmap

A "Do Not Hold" warning system based on historical weekend performance. Input your option expiry date, and we'll calculate projected theta loss versus average weekend volatility. If the cost exceeds the expected move, you'll get a clear warning.

Liquidity Depth Tracker

Real-time order book analysis showing where true liquidity lives. No more getting trapped in phantom liquidity that evaporates when you need it most.

The Verdict: Adapt or Decay

Markets are not efficient, and they certainly aren't fair. The fragmentation between CME and Deribit creates pockets of opportunity for the observant, while the weekend gap serves as a tax on the impatient.

For the modern trader, the edge isn't just in predicting price—it's in understanding the infrastructure. It's knowing when liquidity providers are active, when they're asleep, and when they're charging you a premium for the privilege of trading.

The next time you see Bitcoin "mysteriously" move on a Sunday afternoon with no news, you'll know: it's not a conspiracy. It's just thin liquidity and whale games. And armed with this knowledge, you can structure your trades to avoid being the liquidity.

Remember: In fragmented markets, timing isn't everything—it's the only thing. Trade when the institutions trade. Close before they sleep. And never, ever hold short-dated options over the weekend unless you enjoy watching your premium evaporate.